This is my last email.

It's time to say goodbye.

It’s your last chance to use the FHSSS before the 30th of June.

If you don’t understand it, not sure if you should use it or haven’t even heard about it.

This email is for you.

If the FHSSS doesn’t apply to you, share this email with a loved one, friend, or co-worker.

They will appreciate you showing them how to save $1000’s, if not tens of thousands.

This is where you will save tens of thousands.

The FHBG allows first-home buyers to buy with a 5% deposit and no LMI.

How to qualify?

Earning up to $125,000 as an individual

Earning up to $200,000 as joint applicants

As shown on the Notice of Assessment (issued by the ATO)

If you earn above $125,000 as an individual or $200,000 as a pair…

You can salary sacrifice via the FHSSS to qualify for the FHBG.

A strategic salary sacrifice above the FHSSS can also help you avoid LMI.

Here are two client examples to show you how we are saving clients 10’s of 1000’s in LMI and assisting them with their Financial Planning, Lending, and Purchasing Strategies.

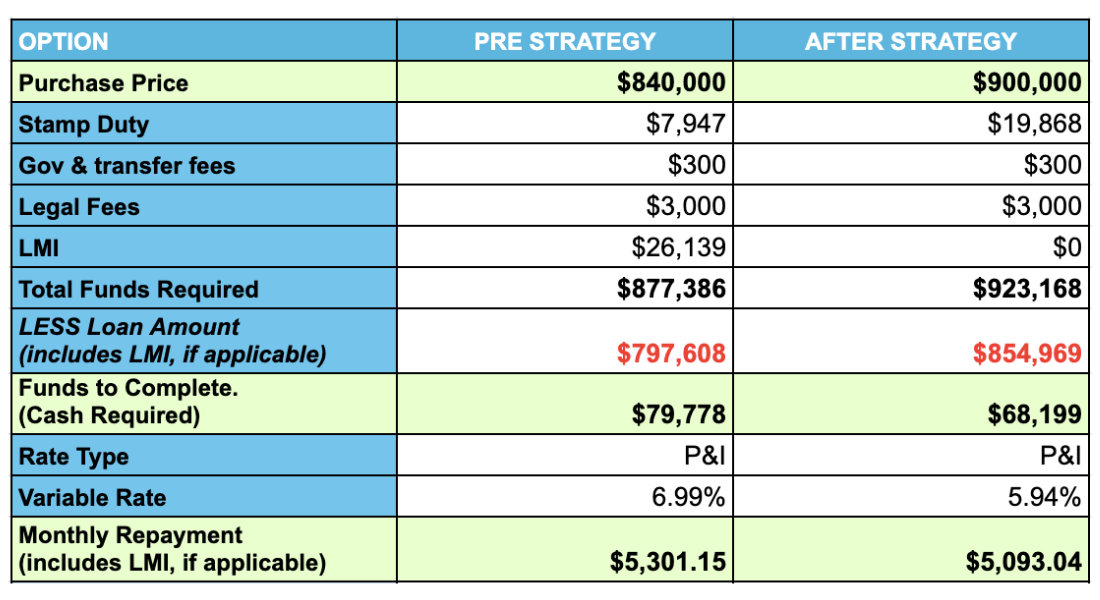

Client Strategy One

Couple earning $221,800

Salary Sacrificing $15,000 each = $30,000 for FHSSS

Income Pre Strategy for 24FY $221,800 (Does not qualify for FHBG)

Income Post Strategy for 24FY $191,800 (Does qualify for FHBG)

The Strategy Result is shown below

$60,000 Potential Purchase price increase

$26,139 in saved LMI

$11,579 in reduced deposit needed

1.05% sharper interest rate

Repayments $208.11 cheaper per month even with the higher purchase price

$12,198 in additional tax savings due to FHSSS

This reflects an immediate $23,777 saving due to the FHSSS and lower deposit needed.

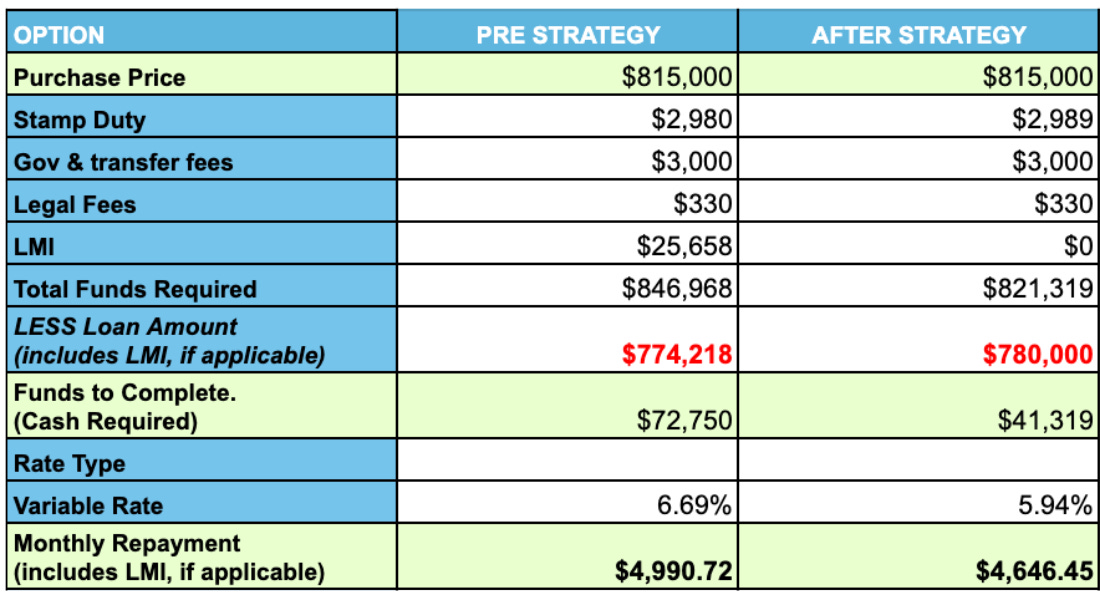

Client Strategy Two

Individual earning $162,500

Salary Sacrificing $15,000 for FHSSS

Using Carry Forward to Salary Sacrifice an additional $22,500

Income Pre Strategy for 24FY $162,500 (Does not qualify for FHBG)

Income Post Strategy for 24FY $125,000 (Qualifies for FHBG)

The Strategy Result is shown below

This strategy is slightly different.

You’ll notice the client is adding $22,500 to their super account, which they can’t withdraw because it’s over the FHSSS limit.

They are investing $22,500 in their super rather than paying $25,658 in dead LMI.

However, this contribution will not be completely lost as it will boost their tax return.

$19,510.50 increase in tax return due to Salary Sacrifice + FHSSS

The client is only $2,989.50 worse off after their $22,500 non-FHSSS Sal Sac.

$25,658 in saved LMI

$31,431 in reduced deposit needed

.75% sharper interest rate

Repayments $344.27 cheaper per month

The client is still immediately $28,441.50, better off.

This email is general in nature.

The above strategies might not suit your circumstances.

FHBG limits will differ outside of Sydney.

In saying that, these strategies might be EXACTLY what you should be doing, and if you’d like us to review them for you, reply to this email or contact us for a tailored approach.

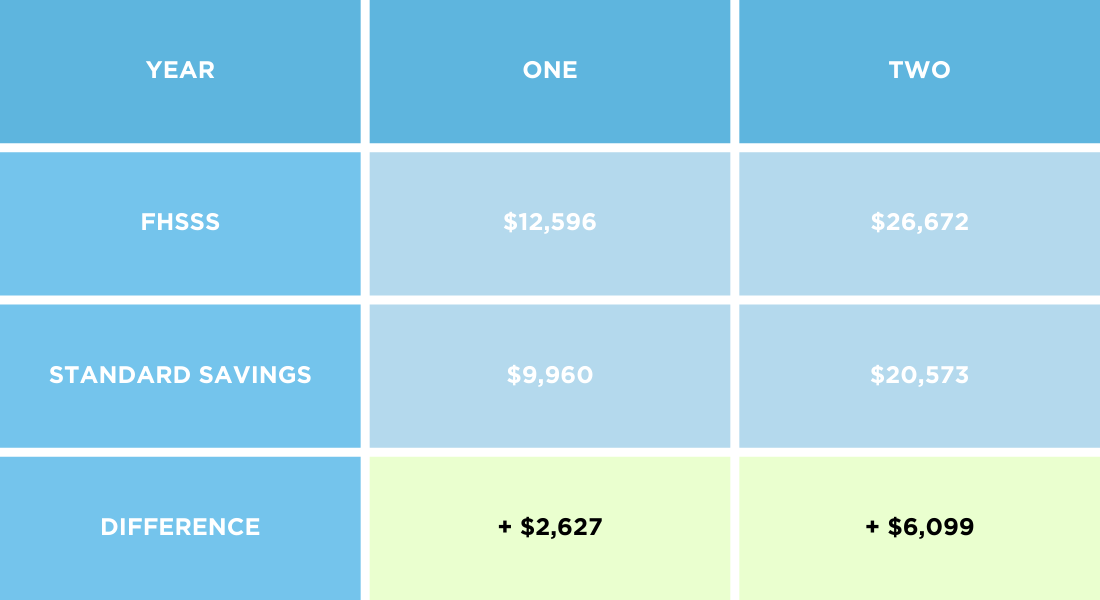

As mentioned, the FHSSS provides tax benefits.

SOURCE: Benefits are even greater if done over 3-4 years.

The above is just free money, even if you use the FHSSS before and After July 1.

Why is this my last email regarding the FHSSS?

We’ve created an FHSSS Course, so we never have to explain FHSSS again.

It’s complimentary.

We know that if we solve your simple problems and save you thousands, we’ll become your unfair advantage and help you save/make tens if not hundreds of thousands.

Ready to work with us now?

Contact us here

Your calculation for FHSSS Tax benefit table for year one doesn't seem to quite add up with 15% after tax. Could you please elaborate where does 13% come from?