Dear Mum

you did the right thing.

When I visit my parents, my mum usually complains about a lot of things. Lately, it's been a constant refrain of, "I wish I didn’t buy this unit and just saved the money or invested it. I would have had more money."

But did she really make the wrong choice? Let’s take a closer look.

The Purchase

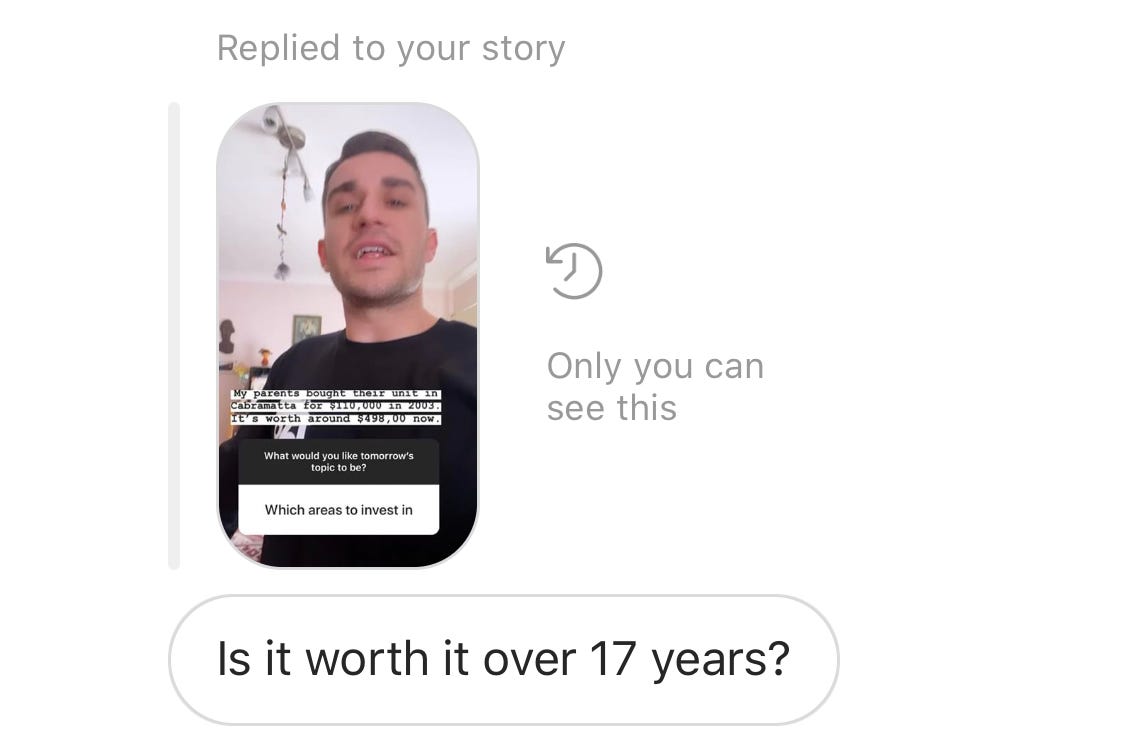

I shared a story on our Instagram about my parents purchasing their home in 2001 for $105,000, which is worth $420,000 now, and I received the below response.

This prompted me to do the math so that you can understand why we’re constantly preaching good property investment, and more importantly, so that my mum stops stressing.

The Mortgage

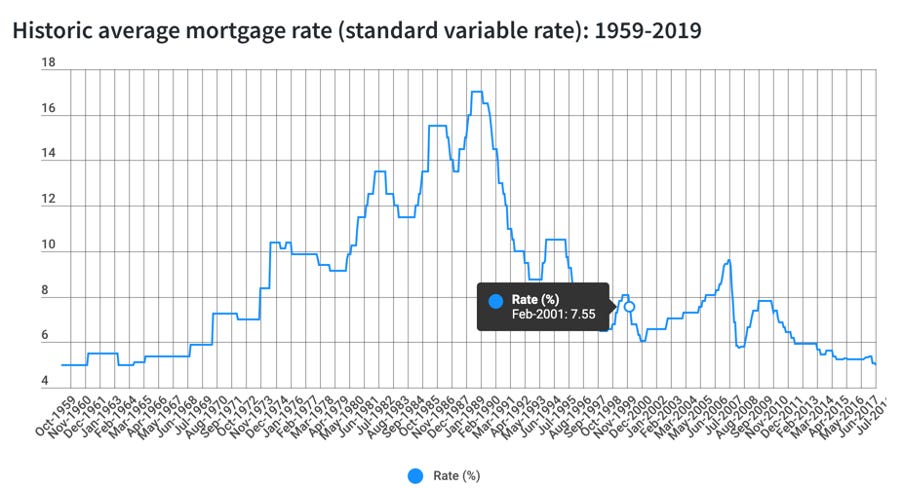

Here’s the historical data on mortgage rates to provide context:

My parent's property was acquired on the 14th of February in 2001, and the mortgage was paid off on the 14th of February, 2013.

This graph is the St George Principal & Interest Graph for this period. I have used the 7.55% interest rate for the loan's lifetime, even though the average rate was significantly lower throughout.

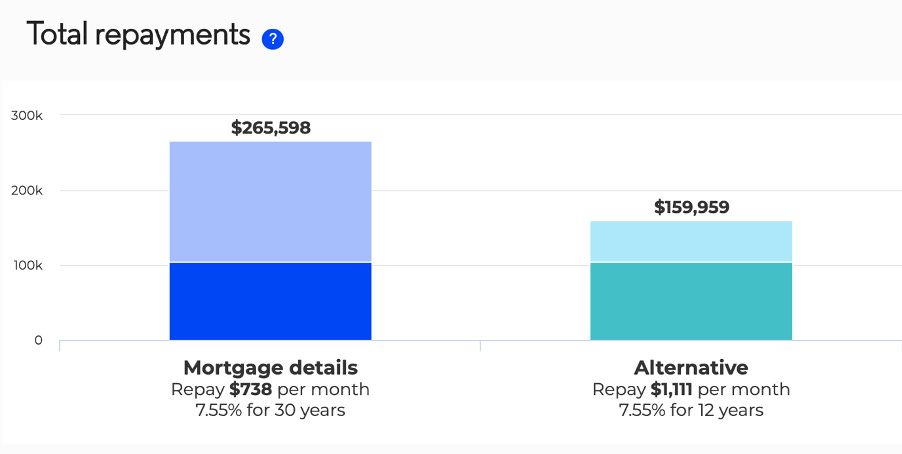

The column on the right shows the total cost of their loan.

$159,959.

My parents increased their repayments, and this is why they were able to pay the loan in 12 years.

This is based on repayments of $1,111 per month.

If they decided to sell their property in 2013, they would have sold it for $294,000.

This is based on an average value, as per Core Logic's average sales for identical units from Feb – Dec 2013.

Minus the agent fee of 2% $5,800, let's say $10,000 if they got ripped off.

Minus the total loan cost of $159,969.

That's a profit of $124,031.

Wait for it.

Tax Free.

Saving

Prior to purchasing their property, they were renting something identical for $640 per month. Rents went up over a 12 year period. For this exercise, we'll just say that theirs didn't.

So, what happens if they invest their mortgage repayment of $1,111 per month minus the rent of $640. (Because they need somewhere to live).

This would mean they have a monthly savings capacity of $471.

3.92% Interest rate based on RBA average of Savings/Term Deposit accounts for date range Feb 01" - Feb 13"

$18,883 Profit.

Before Tax.

There isn't much more to say.

Investing

We have identified that they would have a monthly investment capacity of $471.

It's hard to identify where they would have invested, so in this case, I have selected a commonly used, low-cost retail fund.

The Vanguard Balanced Index Fund.

I subtracted the GFC year, during which we saw a loss of 22.21%, from the calculation because I'd prefer to underestimate.

$39,374 Profit.

Before Tax.

Did she make the right choice?

Profit

Property = $124,031

Savings = $18,883

Investment = $39,374

You tell me.

What mum could have done

Unfortunately, my mum didn’t have a team like us guiding her through wealth during her working life.

If I had been my parents’ adviser at the time, I would have transitioned their only asset into a larger asset and kept the unit as a future downsizer. They could have run the loan interest-only and debt-recycled the funds into a portfolio to create even more wealth.

But even without that guidance, my parents are okay—and they will continue to be okay. This situation serves as a great lesson in understanding the true value of professional advice.

We could have been a wealthy family, but there was no one to show them how.

Now, it’s my responsibility.

And while I might be biased, I think her greatest investment was in raising me.

The data and original newsletter are from 2021, but the principle remains the same.

The unit is only worth more money now.

My mum still complains, just not about me…