Budgets don't work

This is why...

“Can you help me budget?”, “Do you have an app that I can use to budget?”, “Can we work through my spending to ensure I’m not spending too much?”

No.

I understand that many advice offices LOVE putting together budgets and charging ongoing fees to help you “budget”, but I could not think of anything worse.

Budgets are simple.

Money in.

Dedicate a % towards your financial / lifestyle needs, goals and objectives.

Money Out.

We have helped thousands of clients save for a property, get out of debt, position multiple purchases, and invest portions of their salary every paycheck.

Yet, we’ve never had to work through a detailed budget on an ongoing basis.

Why? Because you should know what your expenses are and if you don’t, that’s an exercise you can do yourself.

I could not think of anything worse than calling my clients every paycheck, filtering through transactions and calling them if they spend too much at a store they love or restaurant due to a celebration. 🤮

We have a simple solution. A solution that has helped thousands of individuals manage their money simply yet efficiently.

Want to sort out your $$$$ ?

Grab a paper and a pen.

This one’s for you.

Illustrations by @furrylittlepeach

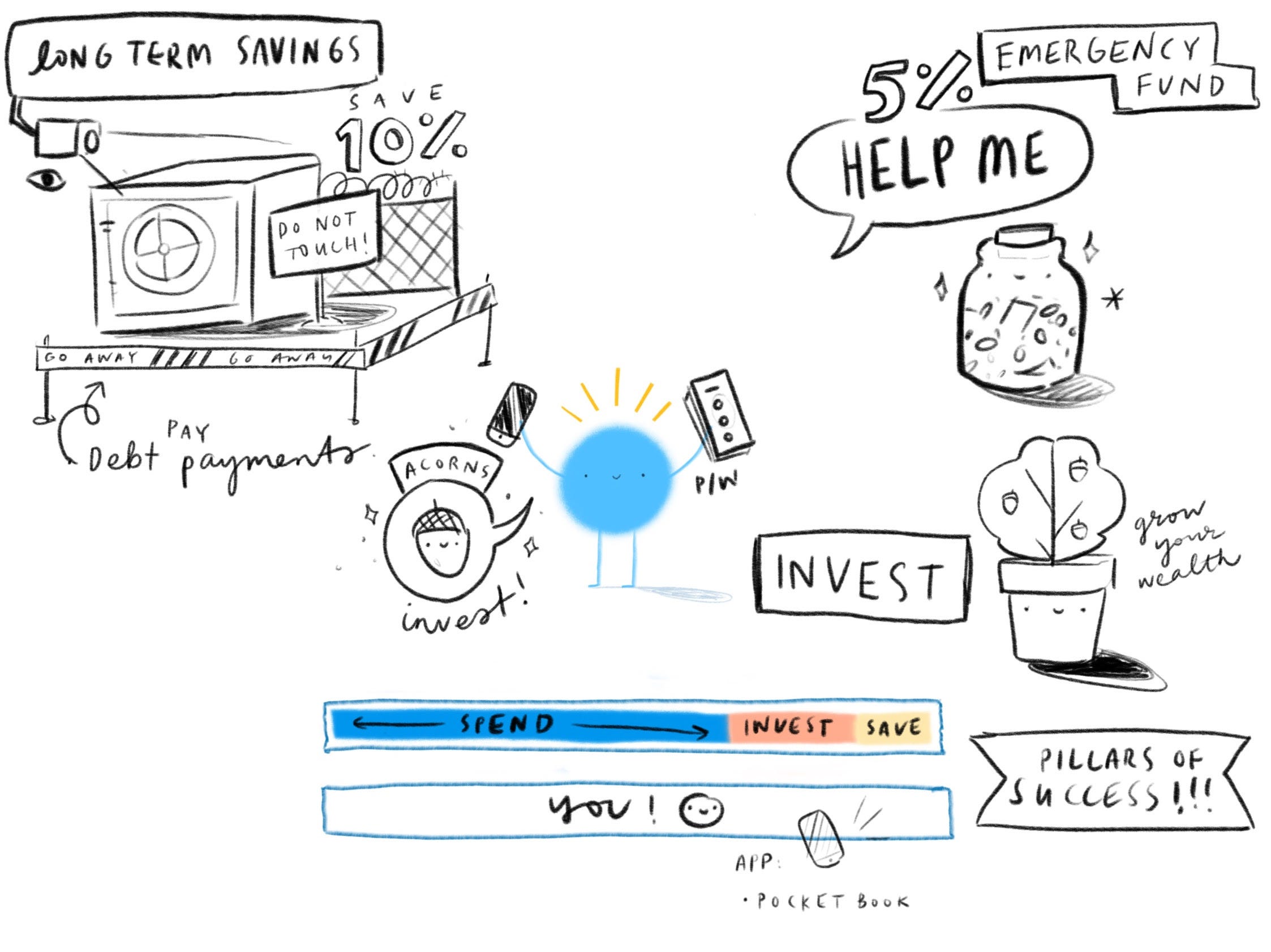

The Money Cheat Sheet

That little blue character. That's you.

Draw your version in the centre of a blank page.

The cash in the hand. Draw that too.

Write what you earn in your bank account after tax per week, fortnight, month, or however you get paid.

Yes. even if you’re self-employed. I feel you.

FUTURE YOU

If you have a mortgage.

Use an offset account linked to your highest interest-charging debt.

Please note that you are not earning interest with an offset but saving interest instead.

Although unlikely, if your savings account rate is higher than the interest charged by your bank, use that instead.

If you don’t have a mortgage.

Find an account that;

pays a high compounding interest rate

has no fees

has no penalties if you don't deposit or withdraw

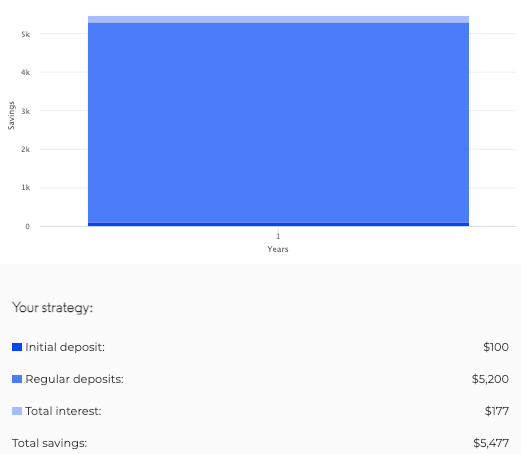

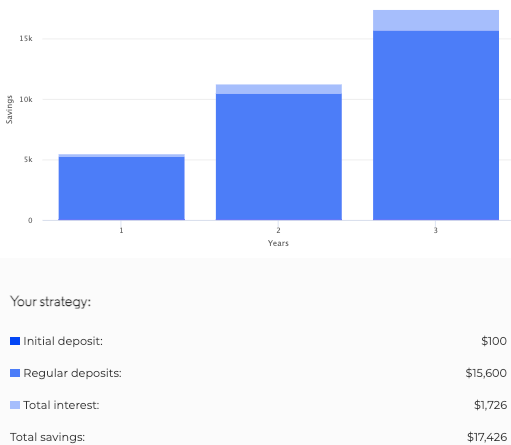

To begin, you will transfer 10% of your total after-tax income into this account.

In this newsletter, we'll use $2000 per week as the working example.

Replace this with your numbers and payment frequency.

We'll use a %

10% of $2000 = $200

$200 gets deposited into this account every week.

This money should not be used for anything apart from long terms savings.

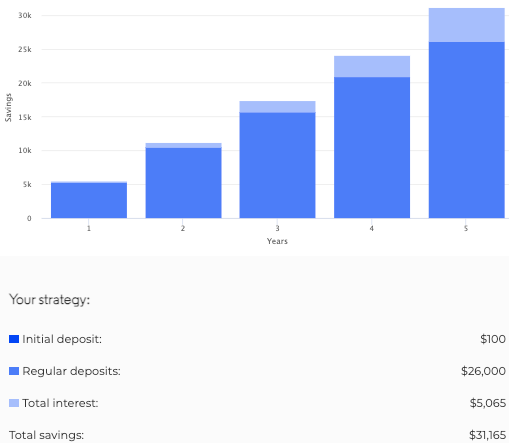

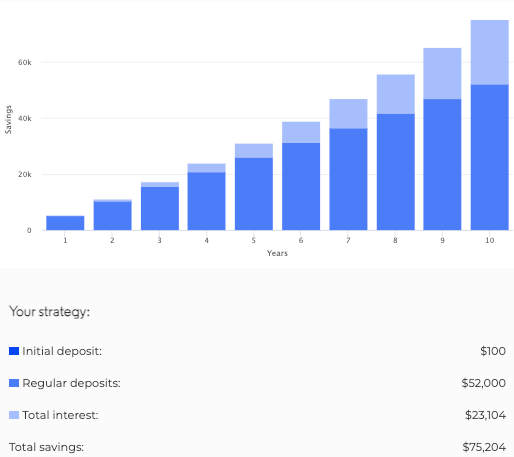

1 year = $10,801 ($201 interest)

3 years = $33,316 ($1916 interest)

5 years = $57,703 ($5503 interest)

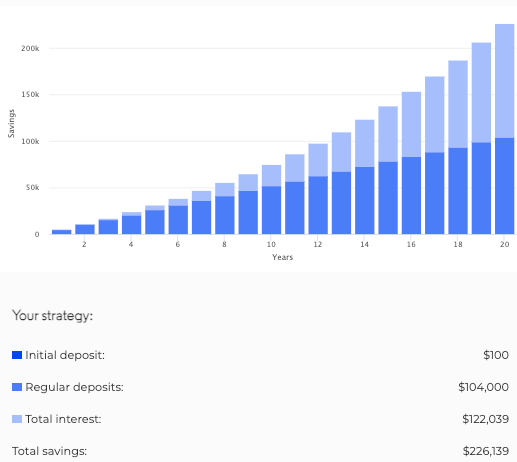

10 years = $127,915 ($23,715 interest)

20 years = $318,316 ($110,116 interest)

Based on a 4% return.

These funds are for future you.

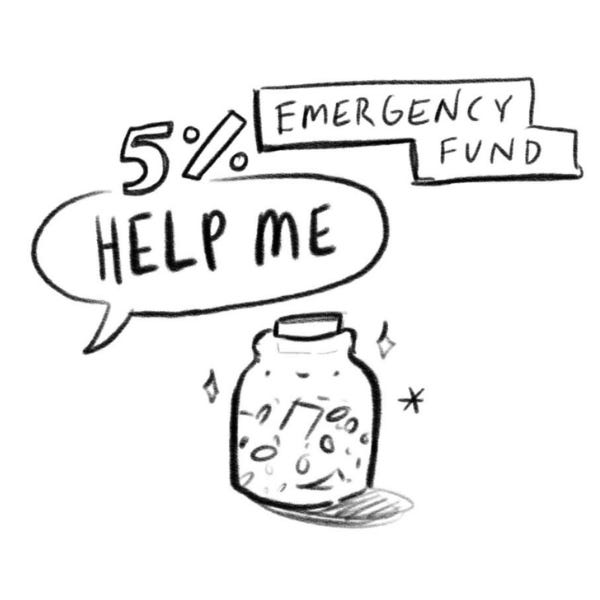

BACK YOURSELF

Building an emergency fund is useful as it ensures that you do not have to touch your long terms savings in the event of an emergency, loss of income or unexpected expenses.

If you have a mortgage, use an offset. If you don’t, you should use an accessible savings account for this.

To begin you will transfer 5% of your total after tax income into this account.

We'll use a %

5% of $2000 = $100

$1000 gets deposited into this account on a weekly basis.

We are working towards acquiring 3 months of income.

Once you've acquired three months of income.

Allocate the 5% towards long-term, investing or treating yourself.

This is the best bit.

If you use any of your Emergency Fund, you don't have to try and pay it back.

Next paycheck, you just continue doing the 5%.

The same applies if your emergency fund isn’t full yet.

MAKE MONEY MOVE

You should be investing some of your income in a regular investment strategy.

Even if you don’t have a large amount to begin. There are micro-investing options such as Raiz, Spaceship, Commsec Pocket, Superhero & Stake to start allocating your money into shares, index funds, managed funds and ETF's from the palm of your hand.

To begin, you will transfer 5% of your total after-tax income into your investment platform of choice.

We'll use a %

5% of $2000 = $100

$100 gets deposited into this account on a weekly basis.

This is an example of using an aggressive allocation based on an average 7% return.

TOO MUCH IN OFFSET, SAVINGS OR EMERGENCY?

Many of our clients transition their long-term and emergency savings into an investment strategy once they have hit an amount that suits their personal and future goals, needs and objectives.

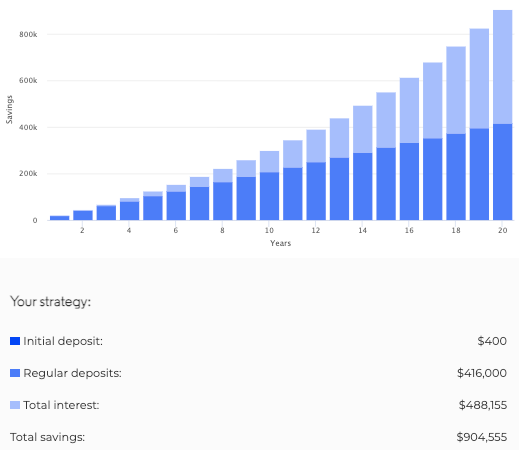

Here is an example of a 20% allocation into an investment strategy over 20 years.

Compounding interest is a beautiful thing.

GOALS OUTSIDE OF THIS

If you are saving for your first property, consider the FHSSS.

If you want to save for things like travel, gifts or a puppy.

Open separate accounts or offsets.

Want a tailored strategy to maximise your savings/ emergency and investment plan?

Contact Us Here

The above email is general in nature. It does not take into account your specific goals, needs and objectives. Before acting on this information, ensure you do your own research. Tools like ASIC's Money Smart Budget tool can help you form a baseline.